ACCA FR(F7)必考知识点 | NCA held for sale 精讲

ACCA考试科目FR(F7)必考知识点,Non current assets held for sale有关的知识点。

对于Non current assets held for sale,它和Non current assets以及Current assets是不一样的。

比如说Non current assets中的PPE,它持有的目的就是作为企业的固定资产,长期持有的。再比如说Current assets中的inventory,一开始的目的就是为了交易而产生的。对于Non current assets held for sale它本身是可以使用很多年的,但是现在持有的时间不足一年了。

所以我们对于Non current assets held for sales是要单独列示在资产负债表中的。

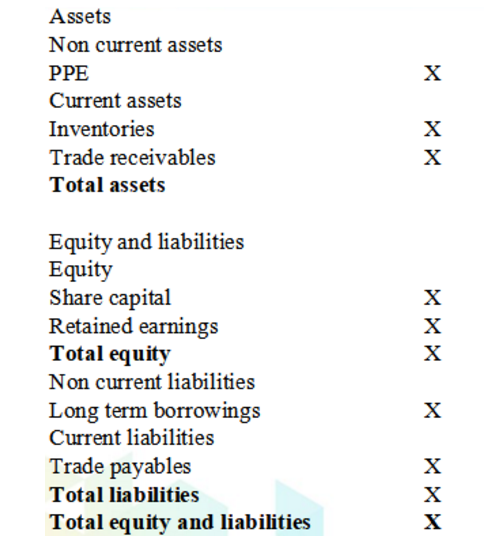

通常我们所看到的资产负债表是这样的:

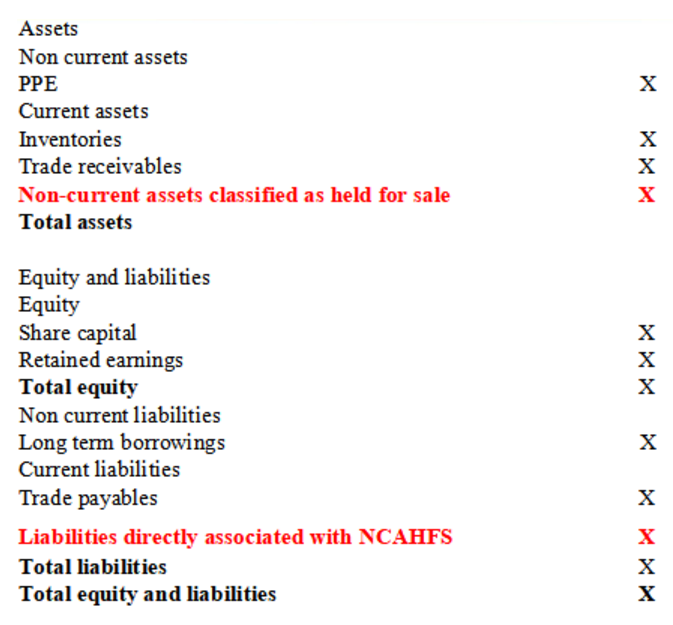

但是有了Non current assets held for sale之后,我们的报表就要变成这样:

所以大家在这里要知道的是Non current assets held for sale是需要单独列示在资产负债表中。

那么什么时候可以划分为Non current assets held for sale呢?它必须满足:

1.对于Non current assets held for sale,它必须是一个销售的交易,而不是持续的使用。

2.The asset must be available for immediate sale in its present condition.在当前可达到立即出售的条件。

3.Its sale must be highly probable.销售是非常有可能的。

那什么情况下,意味着是Its sale must be highly probable呢?

1.Management must be committed to a plan to sell the asset.管理层承诺有计划去卖。

2.There must be an active programme to locate a buyer.已经开展活动,很积极的去寻找买家。

3.The asset must be marketed for sale at a price that is reasonable in relation to its current fair value.资产的售价相对来说是合理的。

4.The sale should be expected to take place within one year from the date of classification.从划分日开始,销售会在一年内完成。

5.It is likely that significant changes to the plan will be made or that the plan will be withdrawn.该计划,基本上不能取消。

这就是highly probable的条件。

在这里,是有2个特殊的情况的:

第一种情况,如果因为不可控的因素,导致已经划分为NCA held for sale的资产,没有办法在一年内出售的,比如说政府出台了政策,导致没有办法再一年内出售了,这个时候,仍然是可以划分为NCA held for sale的。除此情况导致的没有办法在一年内卖出的,就要停止划分为NCA held for sale。

第二种情况,购买这个子公司的目的,一开始就是为了涨价之后再卖出的,那么如果想要在最开始就划分为持有待售,就必须要满足:1-一年内卖出;2-Highly probable的条件要在三个月之内完成。

那么接下来,我们再来看下与Non current assets held for sale计量有关的知识。

大家在这里要注意的是,Non current assets held for sale无折旧,无增值,只减值。

比如说固定资产在2019年6月30日的账面价值是50W,且在这一天的时候,划分成为了Non current asset held for sale。那么这个时候,我们要做的会计分录就是:

Dr NCAHFS 50W

Cr PPE 50W

并且在转为NCAHFS之后,就不能再计提折旧了。

而且NCAHFS它的减值是与众不同的,它是按照carrying amount与fair value less cost of disposal孰低来进行计量的。比如说减值之后的金额是47,那么这个时候,要做的会计分录就是Dr P&L 3 Cr NACHFS 3W,它的减值是要进入到利润表的。